![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

"In the past, the funding needs of tens of millions of small and micro enterprises have always been difficult to meet. With the development of financial technology and policy support in recent years, small and micro enterprise credit has stepped from the edge of the past to the central area. ã€

Text /Andy

Source: P2P Review

In 2017, the Internet financial head platform building block box served tens of thousands of small and micro enterprises and self-employed individuals. The annual small and micro business lending transactions amounted to about 1.5 billion yuan, covering more than 30 provinces and municipalities across the country.

The town where Chen Wei lives is the famous "Knitting Town" in Jingzhou, Hubei Province. The town has opened hundreds of garment factories, large and small, from the embryonic cloth, dyeing to embroidery, printing to needle thread.

|

Chen Wei’s factory has developed rapidly and has gradually grown from a small workshop of more than ten people to an area of ​​over 3,000 square meters.

Chen Wei is also doing garment processing. He thought that labor-intensive business always had to think about some new tricks! As a result, Chen Wei’s factory no longer processed Qiuyi Qiuku, and began to specialize in foreign orders. All the products produced were sold to countries in Europe, Africa and the Middle East through intermediaries. With many years of experience in garment processing and management, coupled with the lack of competitors in the early days, Chen Wei’s factory has developed rapidly. From the small workshops of more than ten people, it has gradually developed into a formal area of ​​more than 3,000 square meters with more than 40 fixed employees. factory.

The boom in business is followed by greater demand. After the machine has been used for more than ten years, the production capacity can not keep up, and the operation ease is not as good as the new machine. "When the monthly production capacity was basically fixed at around 100,000 pieces, I began to realize that I needed to update the machinery and equipment to improve production efficiency and productivity." Chen Wei said that now workers are reluctant to use old machines and are willing to use new ones. He wants to use a factory built with more than 3 million yuan to make a mortgage, but the amount approved by the bank is less than half of the factory valuation. Plus, you update the device in batches, and you don't need to borrow too much at a time.

Where does the money come from?

"Suppliers" in action

By chance, Chen Wei knew about the era of small micro credit information service providers, and he decided to try Internet financing. The building block era and the building block are the same as the building block puzzle group. The former focuses on offline asset discovery and field adjustment, while the latter is responsible for online risk control and transaction matching, and cooperates with small and micro enterprises.

The building block era team made a detailed offline adjustment of Chen Wei's business situation, and then conducted quantitative risk assessment of his company and individual online data through the building block. Chen Wei's financing needs were released on the building block P2P platform. Soon, the borrowing target was full, he obtained 60,000 yuan of matching funds from online loan investors across the country, and solved the cost of replacing some machines.

|

After more than ten years, many old machines and equipment in Chen Wei’s factory are in urgent need of updating.

The investors of the building block platform are scattered throughout the country, which also allows the financing needs of small and micro enterprises to receive responses from investors from all over the world. Among them, investors from Jiangsu, Zhejiang, Beijing, Shandong and other places have contributed the most to small and micro-business financing. In the related transaction volume of 1.5 billion yuan in 2017, Jiangsu investors provided 160.3 million yuan of funds, followed by Zhejiang and Beijing.

For the field, the building block and building blocks used the local IPC micro-credit model. Specifically, it is "cross-validation information." After Chen Wei proposed the financing intention, the loanman of the building block era went to his factory for a field trip, the invoices, the bank flow, the monthly wages of the workers, and the inventory, water and electricity consumption, and the number of machines in the warehouse. Verify and even visit the surrounding factories and upstream and downstream enterprises to understand Chen Wei's situation. This is the first heavy data cross-validation. Combine the information into a table, analyze the repayment ability, repayment willingness and potential risks.

The offline data is then subjected to a second cross-check with the online data acquired by the building block. Then, the quantitative wind control model of the building block will perform a second evaluation of the full set of data and offline evaluation results. In this way, Chen Wei, who meets the requirements of risk control, can release financing information through the building block box platform.

Dong Chun, the founder of the building block puzzle CEO and building block, said that small and micro enterprises are all over the country. If only the online model is adopted, it is easy to ignore many third and fourth lines and villages and towns. Therefore, the Group develops and manages assets through the building block era, and the building blocks realize online wind control and transaction matching, thus supporting the small and micro groups. Under the long-term practice of the Group, Xiaowei's loan service has covered more than 30 provinces across the country, covering not only the first-tier cities such as Beishangguang, but also the third- and fourth-tier cities in Guangxi, Liaoning, Guizhou and Gansu provinces.

|

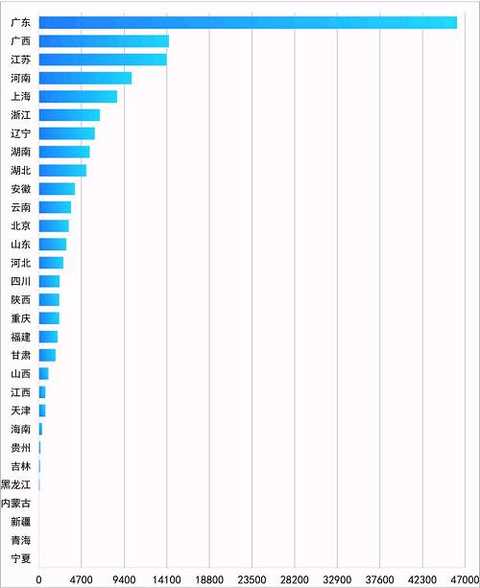

Geographical distribution of loan services for small micro-groups in 2017 building blocks (unit: 10,000)

The vitality of new finance

"Although it has not been completely replaced, but can not worry, a batch of come." Chen Wei got the first money, happy to say. From the time he dialed the loan consultation phone, to get the funds, the speed of less than 48 hours was what he did not expect.

Since 2014, the building blocks have independently explored and served small and micro-business financing. Chen Wei is only a member of thousands of small and micro business owners. According to the Ministry of Industry and Information Technology, as of the end of 2016, there were more than 87 million market operators in the country, and more than 90% were small and micro enterprises. Their needs are equally urgent.

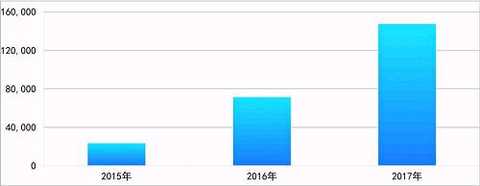

In 2015, the accumulated amount of loans for small and micro enterprises in the building blocks has reached more than 200 million yuan. This amount has increased fivefold in the next two years. In 2017, the platform's accumulated loan amount was about 1.5 billion yuan, serving tens of thousands of small and micro enterprises and self-employed households. At the end of 2017, the balance of loan balance loans exceeded 1.1 billion, covering more than 30 provinces and municipalities across the country.

|

The building block is for the small micro group to accumulate the amount of borrowing in the current year (unit: 10,000)

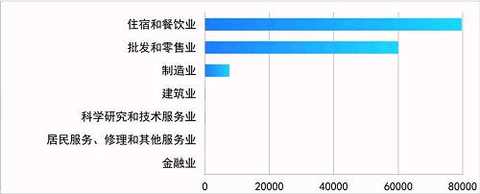

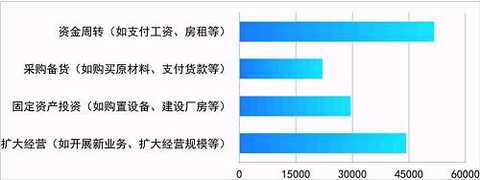

According to the data of the building block, the small and micro enterprises that it serves include grassroots industries that are difficult to obtain credit support from traditional financial institutions, such as small and medium-sized manufacturing, wholesale and retail, accommodation and catering. Under the big data control of the building blocks and the building blocks, these small and micro enterprises have obtained emergency funds and large funds, and played a key role in capital turnover, expansion of operations, procurement and stocking.

|

The situation of the borrower in the 2017 building block for small and micro-group borrowing services (unit: 10,000)

|

The use of lending funds for the loan services of small and micro groups in 2017 (unit: 10,000)

From the edge to the center

From financing nowhere, to building financial boxes through the Internet financial platform, and financing the investment users with financial needs, Chen Wei has updated the old equipment in batches in recent years, and the company is on the right track. The building blocks to meet the financing needs of small and micro business owners through the platform and the financial needs of investors are actually a supplement to traditional finance.

In the past, the capital needs of tens of millions of small and micro enterprises like Chen Wei have always been difficult to meet. With the development of financial technology and policy support in recent years, small and micro enterprise credit has stepped from the edge of the past to the central area.

|

From Chen Wei’s loan consultation telephone number, to get the matching funds, the speed of less than 48 hours was what he did not expect.

On March 19, the China Banking Regulatory Commission issued two documents, respectively, to propose new requirements for the three rural and poverty alleviation financial services and small and micro enterprise financial services, including single-funded credits of less than 10 million yuan (including) small and micro enterprise loans increased year-on-year. The speed is not lower than the year-on-year growth rate of various loans.

On March 28, Premier Li Keqiang presided over the State Council executive meeting to further improve the tax system, support the development of the real economy such as manufacturing and small and micro enterprises, and continue to reduce the burden on the market. It is expected that the tax burden of the market will be reduced by more than 400 billion yuan.

With the official support of the state, the traditional financial industry has also begun to exert its strength. In the new banking environment, many banks are undergoing retail transformation and actively exploring the path of bank micro-financial intelligence.

Take Shanghai Pudong Development Bank Co., Ltd. with 600,000 shares and Ping An Bank, 000001. Starting from 2017, Shanghai Pudong Development Bank and Aerospace Information 600271, the launch of the "Pufa Nonuo Silver Tax Loan" for small and micro enterprises, as long as the application for tax in accordance with the law, there is a fixed business location, no substantial bad credit records can be online real-time Application. Ping An Group's KYB project is in-depth cooperation with MIT to help small and medium-sized enterprises to finance with new artificial intelligence technologies such as big data, biometrics and voice image processing.

On March 19, the data released by the China Banking Regulatory Commission showed that as of the end of 2017, the national small and micro enterprise loan balance was 30.74 trillion yuan, a year-on-year increase of 15.14%, which was 2.67 percentage points higher than the average growth rate of various loans; 152.092 million households, an increase of 1,598,200 households over the same period of the previous year.

Money is pouring into the real economy and is more valuable. In the upcoming policy, there will be more companies joining the inclusive finance industry. Located in the “replenishment†of traditional financial services, the building blocks are still moving forward, using online and offline combination to sink financial services into a more blank market for financial services.

Dong Jun said: "Compared with large-scale enterprise financing, the risk of small micro-credit is relatively high. We must control risks and prevent risks from the front-end to the back-end, so that we can control the risks. We have this. Patience, but also this strength to build a class IPC risk control system for a long time, to serve small micro credit needs."

The fire of the stars can poke the original, and the fire of the stars is the original.

This article was first published on WeChat public account: P2P comment. The content of the article belongs to the author's personal opinion and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk.

(Editor: He Yihua HN110)

Fancy Yarn,Polyester Tape Yarn,Blend Yarn,Twisted Polyester Yarn

ZHANGJIAGANG WELLHOW TRADING CO., LTD. , https://www.wellhowyarn.com